Goods & Services Tax (GST) was a consumption tax in Malaysia which was in effect from April 2015 to May 2018. While it was short-lived, it has many interesting aspects to its design that are worth discussing, especially as talks of GST’s return heat up. One of those interesting aspects of GST is the handling of trade debts.

In this blog post, we will look into how GST from trade debts is handled, along with any possible adjustments, to better understand GST’s inner workings.

Accrual Basis

Most businesses after registering for GST would use the accrual basis for account GST from trade debts. This meant that output tax on debtors was claimable on:

Payment received date if it was earliest of invoice date & goods delivery date

Invoice date if an invoice was issued within 21 days of goods delivery

Goods delivery date if none of the above applied

The date used would be called the “date of supply”. Notice that the payment received date isn’t always the date on which output tax is claimed. In practice, payment is rarely received earlier than the invoice date or goods delivery date, making the payment received date even less used as the time of supply.

As for output tax from creditors, the invoice date was used with no exceptions. This method of accounting GST from trade debts aligns with common accounting practices and was designed to integrate with current accounting practices smoothly.

However, Royal Malaysian Customs Department (RMCD) also recognizes that some small businesses do not use an accrual accounting basis, hence they created an exception that allowed small businesses to use the “payment basis” of accounting for GST.

An application must be made with RMCD and they will review each application individually with certain guidelines to become eligible. The criteria are as below:

i. Annual taxable turnover must be less than RM1 million

ii. Sales were mostly for immediate cash (min. 80%)

iii. No policy of extending credit and collecting debt

iv. Supplies were high-volume and low-value items

v. Capital was not heavily relied on for making supplies

vi. Cash accounting basis was during the normal course of business

vii. If applications were accepted, the business will account for trade debt output & input tax viii. when payment was received & made respectively. This aligns with the cash accounting basis and eases administration for small businesses.

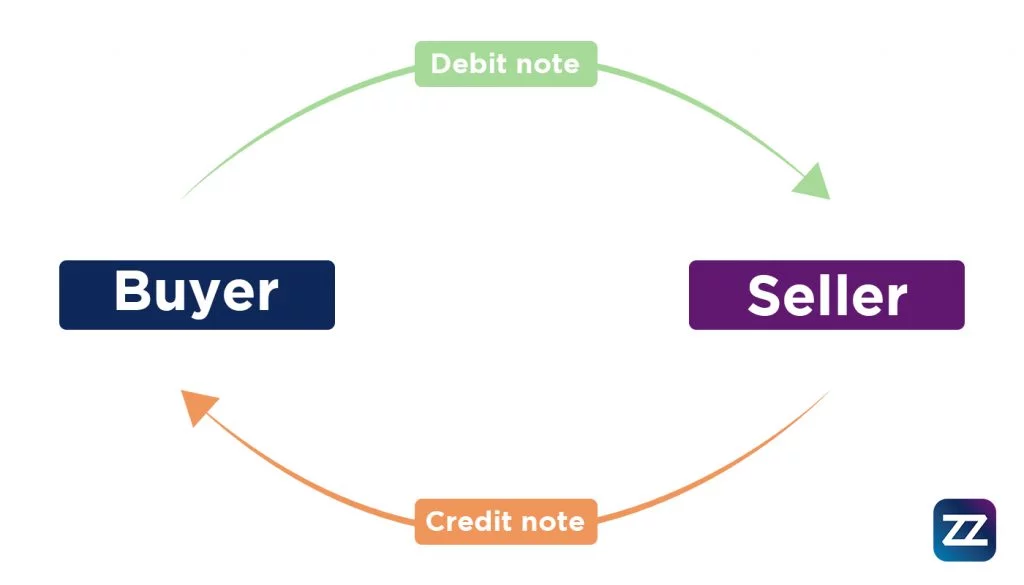

Credit notes & Debit notes

GST’s use of an accounting basis that matched a business’s normal policies was splendid, but there are also certain scenarios in practice that must be provisioned, such as the issuance of credit notes & debit notes.

Credit notes are used to reduce the charge on an invoice, be it for goods returned or overcharging for services rendered. RMCD allowed the transacted amount (along with GST attached) to be reduced. For the supplier issuing the credit note, this meant a reduction of output tax, while the customer had a reduction of their input tax.

Debit notes are the opposite of credit notes, issued when the original supply was undercharged and an increase in the transaction value (along with attached GST) is needed. The treatment was much the same but in reverse, where the supplier issuing the debit note will have increased output tax, and the customer will have more input tax.

However, RMCD also introduced anti-abuse regulations, blocking credit notes & debit notes which were not in the normal course of business. They had mandated that the issuance of credit notes & debit notes must be genuinely for business purposes to be allowed the adjustment.

Bad debts & overdue debts

Of course, that was not the only GST adjustment. Another fairly common scenario is debts long overdue. This GST adjustment clawed back GST until payments were made to settle the debt, in which case the GST clawed back will be re-awarded proportional to the debt settled.

Bad debts were defined under GST as receivables unpaid for 6 months after their date of supply, or when the debtor became insolvent. A negative output tax figure was charged into the GST statement proportional to the % of debt outstanding. If the debtor pays back the debt, output tax would then be accounted for again for the period the customer pays back.

For payables long overdue (6 months from invoice date), businesses must have their input tax credit reduced for the period, again also based on the % of debt outstanding to its suppliers. If the business finally pays the supplier, then they are allowed to claim the input tax credit once again.

The adjustment also accounted for credit notes & debit notes issued previously, appropriately reducing or increasing the GST amount stated in the original invoice.

Summary

The workings behind GST to make it all function are quite complex yet simplified enough to fit neatly with common accounting practices. Some anti-abuse legislation is imposed, but overall, it’s quite transparent with what you should & shouldn’t do with GST. Regardless of if GST is reimplemented in the future, the prevailing consumption tax would benefit from taking over this characteristic from GST 1.0.

Disclaimer

All content provided on this blog is for informational purposes only. The owner of this blog makes no representations as to the accuracy or completeness of any information on this site or found by following any link on this site.

The owner will not be liable for any errors or omissions in this information nor for the availability of this information. The owner will not be liable for any losses, injuries, or damages from the display or use of this information.

References

GST payment basis: Jeyapalan K. (2015), A Guide to Malaysian Goods and Services Tax, McGraw-Hill Education (Malaysia) Sdn Bhd

GST adjustment: Richard T., Thenesh K. (2014), Malaysia Master GST Guide 2014, CCH.